The previous week was absolutely rich in fundamental points of view and many outcomes. In our regular weekly macro report, we will focus on Fed hikes decision and forward guidance, as well as new GDP figures and current inflation expectations from Michigan University. We also comment on our portfolio movements and select possible trades based on appropriate risk/reward.

Previous asset movements

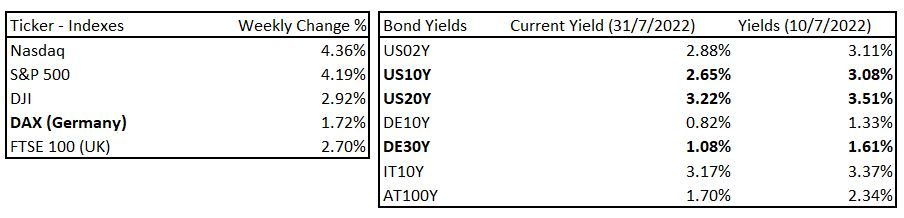

In the previous week, we faced a strong stock market rally. It was caused by many fundamentals, but the main factor was the Fed’s new updates on its forward guidance policy. In the previous macro reports and weeks, we have been strongly confident in a possible bond market rally. Bond yields are falling significantly, so prices and ETFs rose, according to our notes in trading ideas in the previous weeks.

The latest asset movements, Source: Investro analytics team

The Fed hiked by 75bps, but updated forward guidance mattered more

As the title indicates, the Fed did not surprise the market with an unexpected hike. The market mainly expected 75bps and there has been little probability of a 100bps hike. The most important part was delivered at a press conference and include updates on forward guidance. J. Powell said this important note:

‘‘We are now at levels broadly in line with our estimates of neutral interest rates, and after front-loading our hiking cycle until now we will be much more data dependent going forward.’’

As one of our authors mainly focused on the Fed’s neutral rate in the middle of June on the strategy of being long on bonds with long-term maturities, we will easily determine why it is so important:

“The neutral interest rate may help the Central Bank make monetary policy choices by indicating whether its interest rate policy is boosting or contracting the economy.”

“Alternatively, a neutral rate can be considered a possible long-term rate if CB’s targets are fulfilled. However, inflation shocks can cause the overcoming by short-term rates (yields or FFR), but not for long. Because when it happens, something in the economy can break easily.“

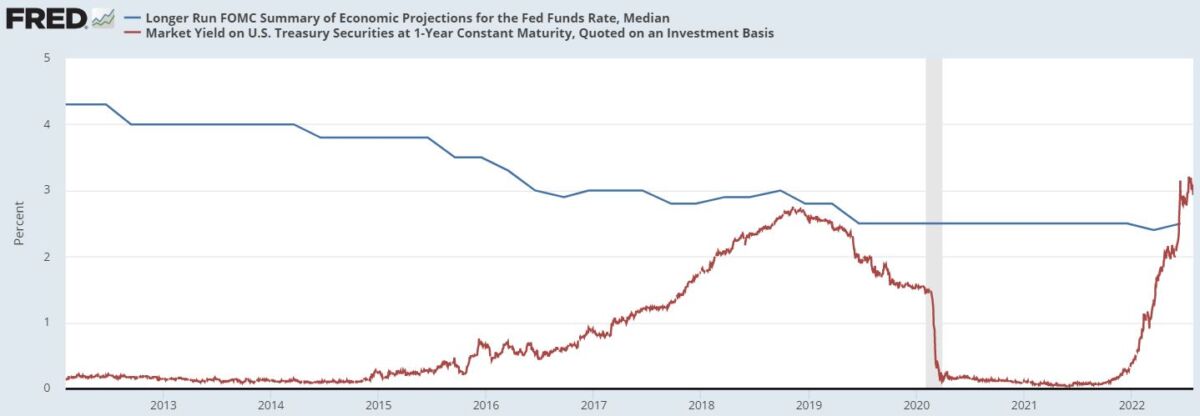

According to our team, the neutral rate can be set up as the long-term projection rate from Fed in dot plot. From the June meeting, it currently stands at 2.5% (in line with fed talks), while market yield on US Treasury Securities at 1Y maturity stands at 2.93%.

Fed´s neutral rate vs. US01Y, Source: Investro analytics team via FRED

In other words, the current Fed Funds Rate is in the 2.25-2.50% range, which is consistent with the Fed’s long-term FFR projection. Its rate, where the economy could reach its potential GDP output. J. Powell was also unable to give some answers to journalists’ questions on bond market pricing (which prices in rate cuts in 2023) and said that it will be data dependent. It means that after reaching the neutral rate, the Fed will still be hawkish and raise rates, but the shocks probably will not be as significant as the hikes in the previous meetings.

You may also like: Amazon had a good quarter

Hikes into the recession

FFR are in the range of 2.25 – 2.50% and currently stands at 2.3% (monitored by effective Fed funds rate), while futures expectations on rates in December 2022 are 3.24%. The difference between them shows us the additional rate hike expectations among market participants. These participants anticipate only 0.75-0.90%, or 3x-4x 25bps, rate increases until December 2022. It shows us, that the market believes that the Fed will not be as aggressive as it was in the previous three meetings.

Spread between futures (in Dec 2022) and EFFR, Source: Investro analytics team

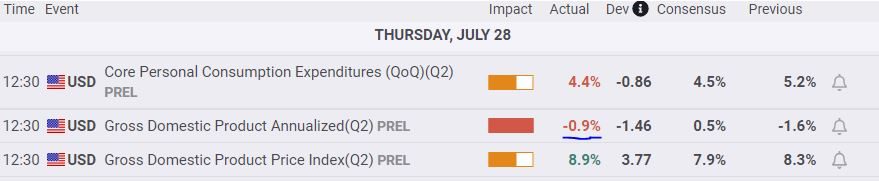

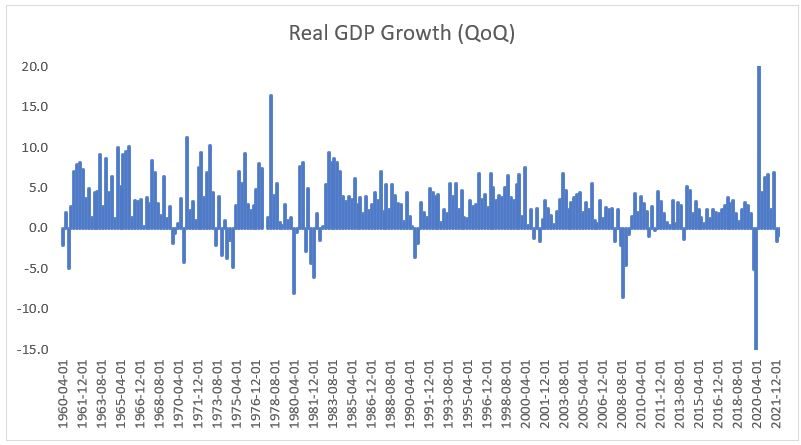

According to the fresh preliminary figures from the US real GDP from the 2nd quarter, where QoQ resulted in a negative figure of -0.9%. This confirms the term of technical recession. The previous figure was -1.6%.

Economic calendar, Source: Fxstreet

However, a similar pattern occurred in 2020, due to COVID-19, later in 2008, and in 1990. We do not know the further figures, but many leading indicators, as PMI suggests, it will not be a great comeback as we saw in 2020. It is due to the still increasing inflation rate and monetary policy tightening conditions. The final results (-0.9%) had been much closer to Atlanta Fed GDP (-1.7%) forecast than the classic consensus (+0.5%). Yes, thus is confirmed, the Fed hikes into a recessionary environment (in a technical way).

Real GDP Growth QoQ, Source: Investro analytics team

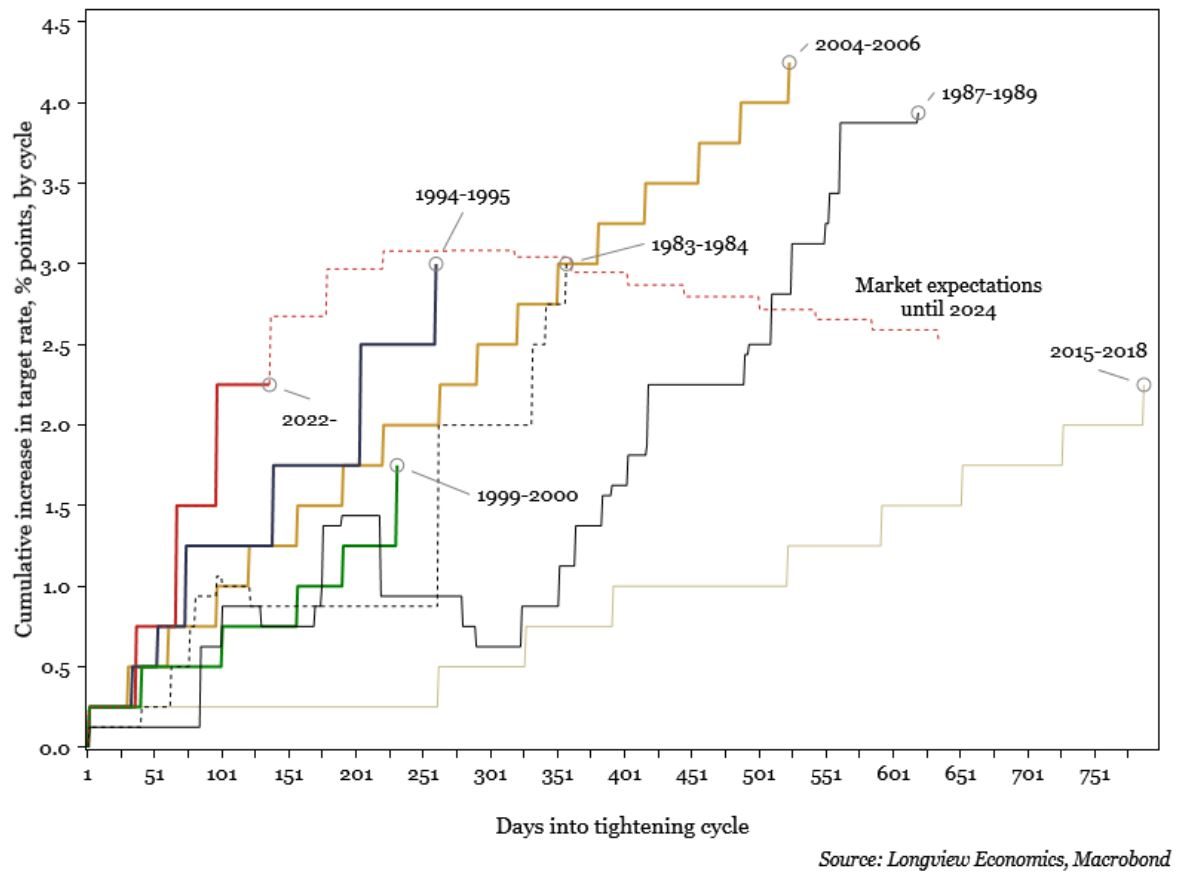

In the chart below from Longview Economics, we can see that the 2022 tightening cycle is one of the fastest, and it took less than half a year since the first hike to now. In the current environment, you just cannot be bullish on stocks. However, the market now fully prices in rate cuts in 2023. The problem is that, despite inflation expectations being slightly falling, the outcome could be worse. If inflation does not slow down in July or August prints (based on MoM), the Fed will hike aggressively and it would be more intensive than current market pricing. However, because the Fed primarily acts on lagging indicators such as CPI and employment figures, there is still a chance that rate hikes will be aggressive in the near term.

Days into tightening cycle, Source: Longview Economics via Macrobond

As we believe that shocks to the economy will reduce the demand side of inflation, the supply side can be impacted only indirectly. We believe the likelihood of this scenario is at 35% (for a more aggressive stance from the Fed).

Read also: Iran’s oil export revenues up 580%

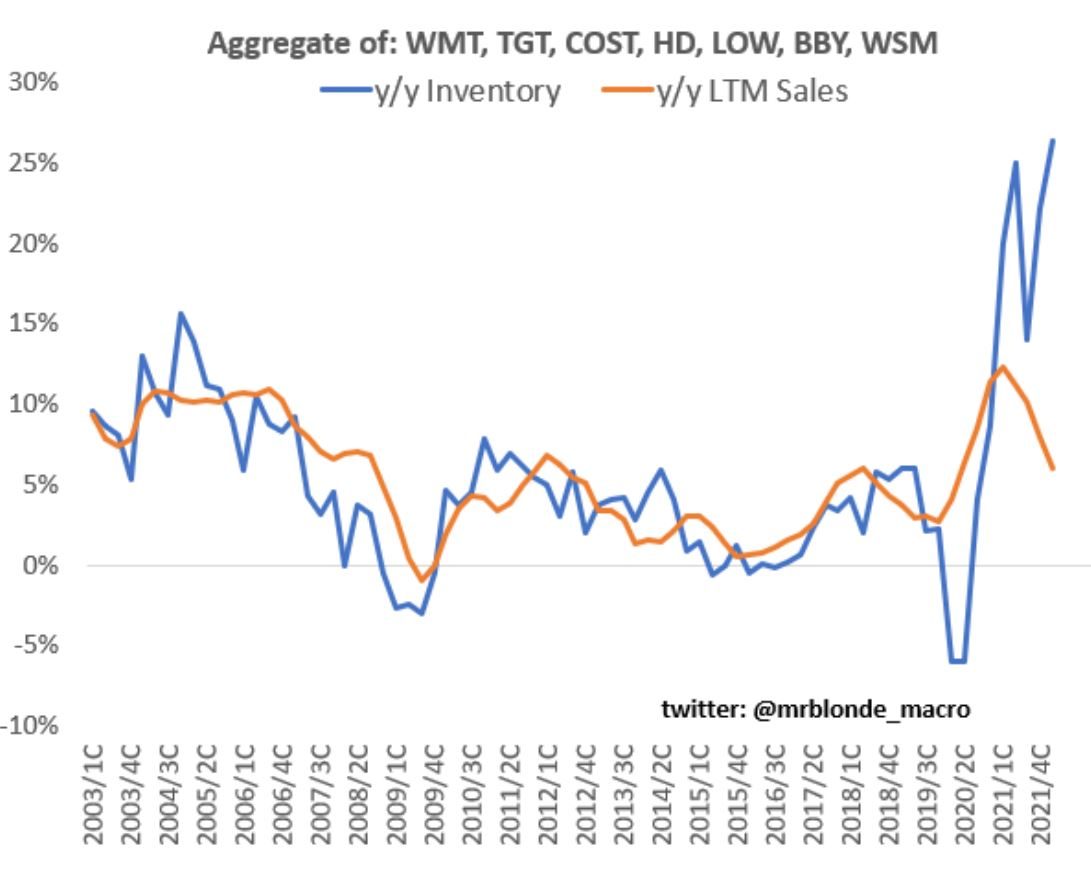

There are not only a plethora of negative consumer confidence and sentiment data that point to low consumption. There are also massive increases in inventories (YoY%) in companies like WMT, TGT, COST, HD, and others. These companies show general oversupply for most of the companies (depending on the sector). It implies that to sell these inventories successfully, these companies need to reduce their margins (to be able to find the demand) and so their EPS.

Aggerate of: WMT, TGT, COST, HD, LOW, BBY, WSM inventories (YoY) and LTM Sales (YoY), Source: @mrblonde_macro

Inflation expectations

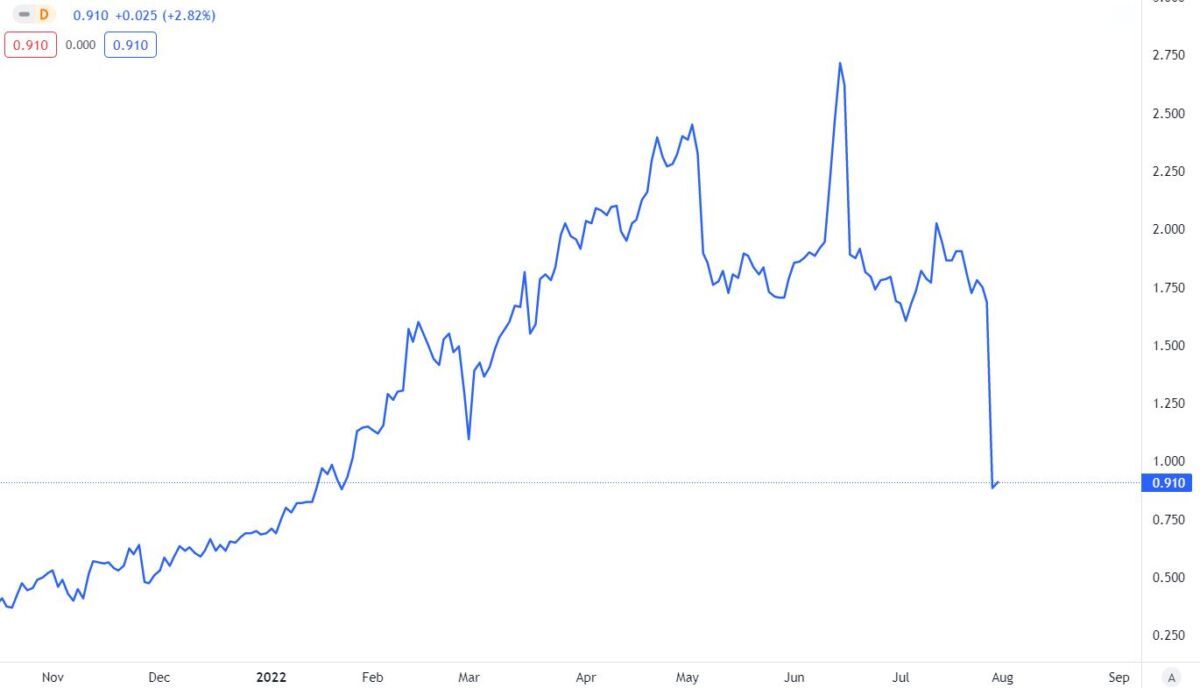

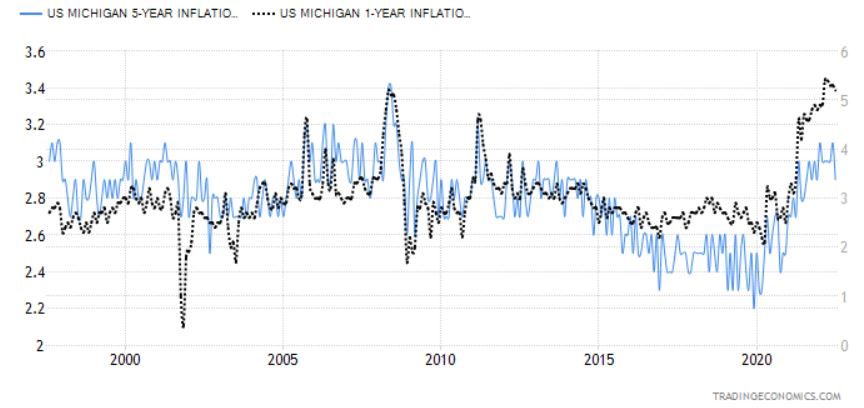

We would point to the most current release of inflation expectations from the University of Michigan for July. While 1-year inflation expectations dropped only slightly, a bigger drop could be seen in 5-year inflation expectations. It is still elevated but is slowly getting under control. While 1Y is more affected by the base effect. The general results are quite positive and tell us the Fed can not be so aggressive because medium-term inflation expectations are starting to slow down.

Inflation expectations measured by the University of Michigan, Source: Tradingview via the University of Michigan

Trading Idea

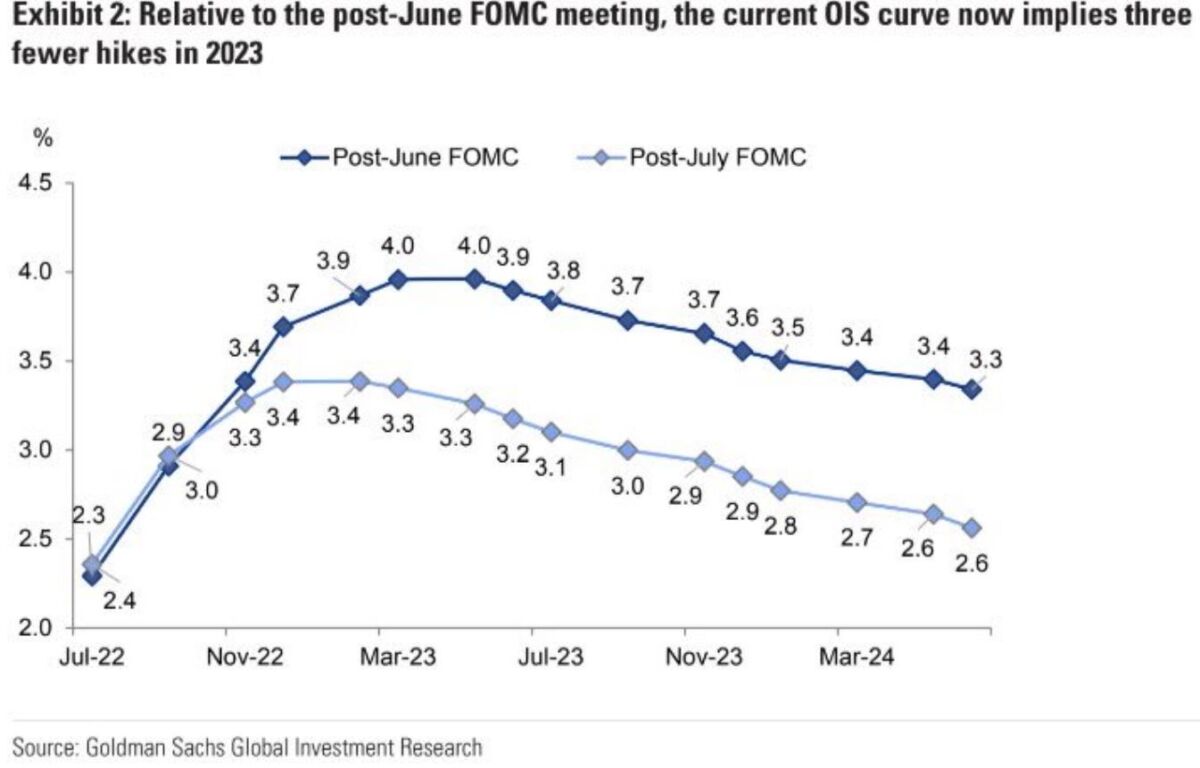

We have identified nice gains in our bond portfolio with long-term duration. We are still very bullish for bonds with long-term maturities, mainly in the USA, but also in Germany. It is mainly due to strong recession fears and expectations of lowered growth and the potential for the Fed to cut rates in 2023. However, look at the pricing of OIS Curve right after the June and July meetings. The expectations for rate cuts in 2023 have significantly increased. This can be measured by the OIS curve as well as from futures.

OIS curve, Source: Goldman Sachs Global Investment Research

We are still bearish on oil, but it is better to be more defensive here as there are many different factors on the way. However, we believe that lowering the PMI with a combination of high inflation and a tightening environment will result in lower demand for oil products. We can also be wrong about oil, so it is better to be defensive.

In the case of stocks, the best scenario right now is to be aside or to focus on proper stock allocations. However, the market rallied on the latest information about forward guidance (will depend on data). The EPS decline, as well as margin reductions, should still show up in the next quarter. We are neutral here, because we see that the situation can be much worse, but also represents a solid situation for long-term portfolio allocation. However, even still, the continuing tightening cycle (slight or aggressive) will lead to lower consumption and thus margin and EPS reduction. From this point of view, we do not see proper long set-ups for stocks, only in the case of stock allocation based on proper sector and industry analysis.

Warning: The fully covered text is not investment or trading advice. It represents only the author’s point of view and thoughts, and we do not bear responsibility for your potential loss. The article serves only for analytical and marketing purposes.

Comments

Post has no comment yet.