In the previous macro report, we focused on the European energy issue, which is leading to higher inflation, real GDP reduction, as well as consumer destruction and the increase in recession likelihood. Today we will provide some interesting charts representing that our opinion could be right and how to trade current circumstances.

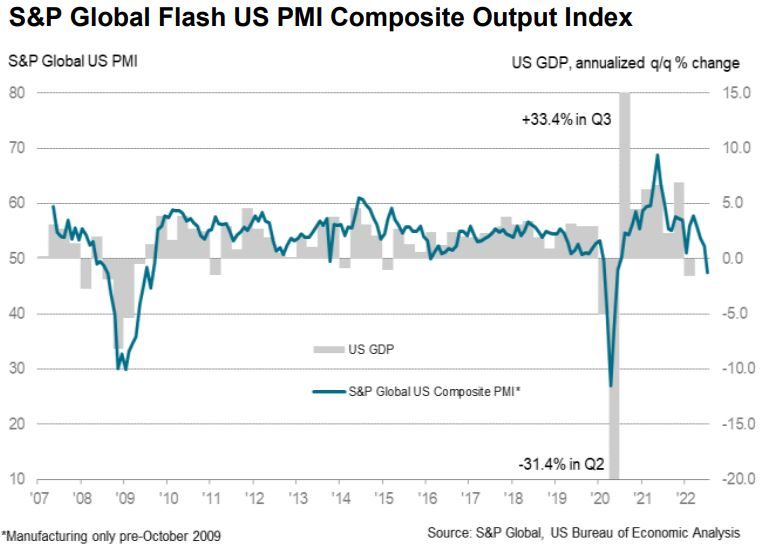

US PMI under the expansion 50

On Friday last week, the flash for the S&P Global Flash US PMI for July was released. The outcome is a little bit surprising for the market, but not for us. We have been warning for weeks about the economy’s slowdown. The Flash PMI simply confirms our previous weeks’ thesis. Here are the flash results for June:

- Flash US PMI Composite Output Index at 47.5 (June: 52.3). 26-month low.

- Flash US Services Business Activity Index at 47.0 (June: 52.7). 26-month low.

- Flash US Manufacturing Output Index at 49.9 (June: 50.2). 25-month low.

- Flash US Manufacturing PMI at 52.3 (June: 52.7). 24-month low.

In both 2008 and 2020, the readings under 50 represented no room for expansion, and it is less probable to revert this trend in the short-term.

S&P global flash US PMI composite output index, Source: S&P Global, US Bureau of Economic Analysis

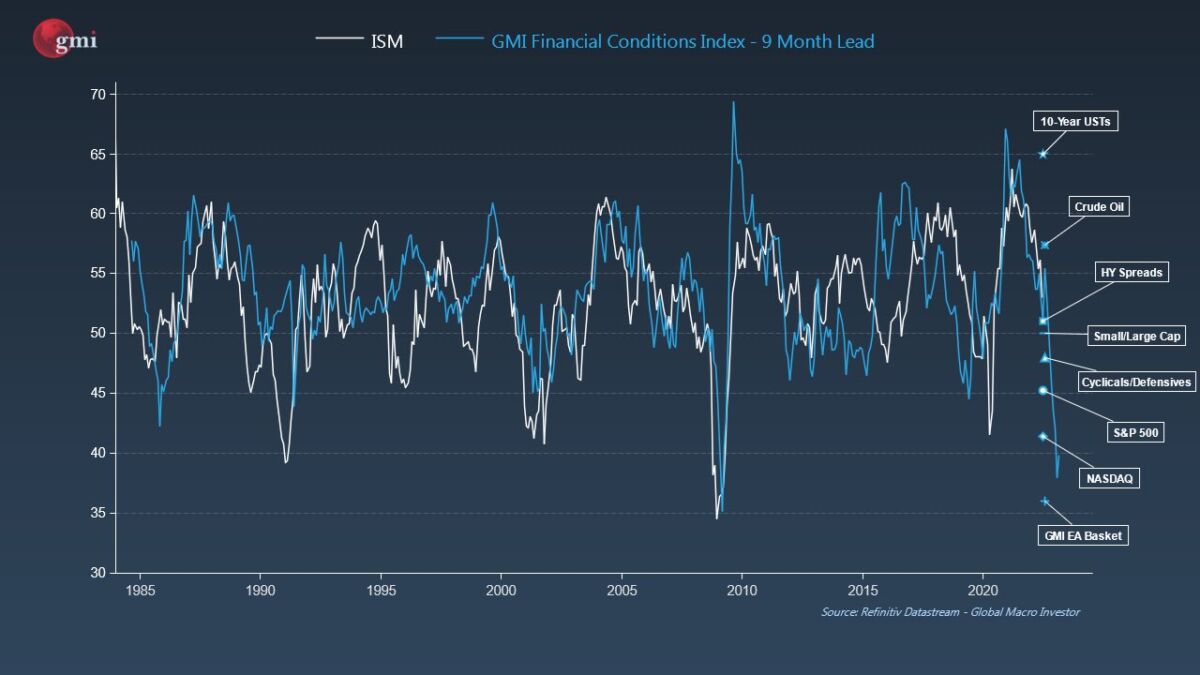

Now I would like to point out the great model from Global Macro Investor, which released its own model to predict the further PMI based on logical inputs. For 9 months, the GMI Financial Condition Index has led over ISM.

GMI financial condition index, Source: Julien Bittel via Twitter, Global Macro Investor

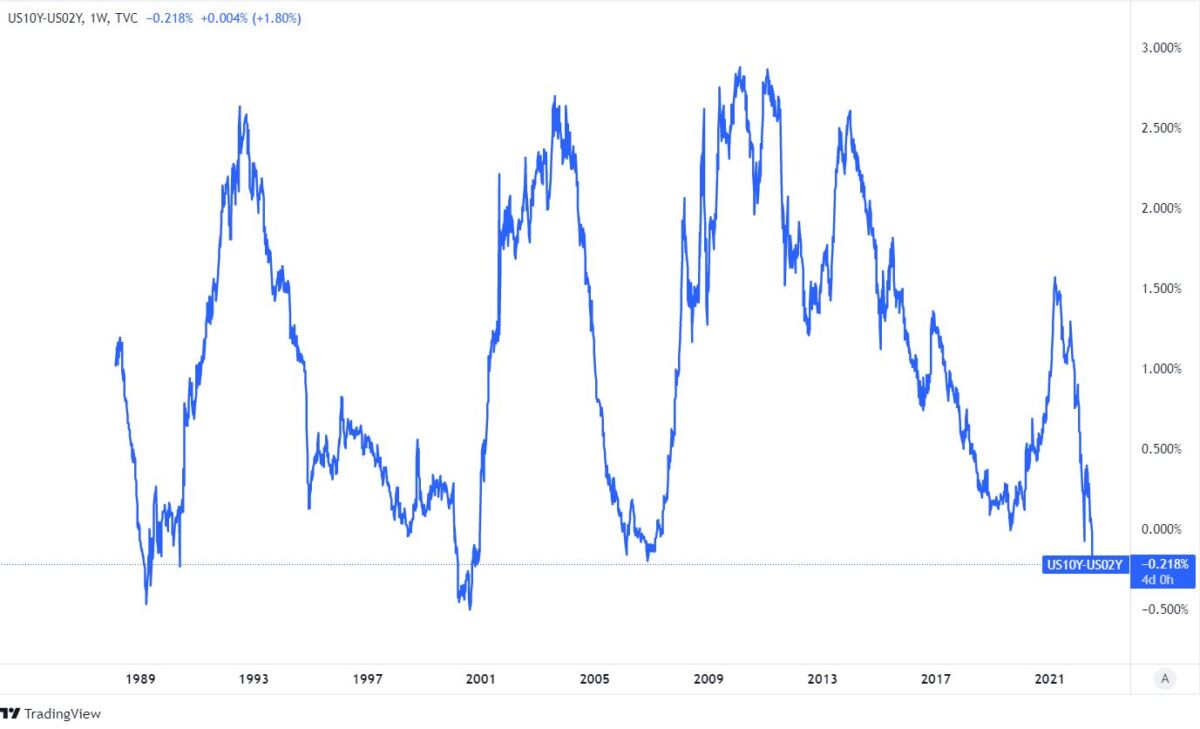

The yield curve inversion shows no room for growth as well as new orders

As the short-term yields, or the front-end of the yield curve, mainly represent the monetary policy implications, the back-end, or the long-term yields, are more focused on economic growth and long-term inflation expectations. As short-term yields are higher than long-term ones, like right now, the market expects an economic slowdown. This was seen before the crises – 2000 and 2006 – and many times before. And now. The bond market is fully ignoring the Fed, its projections, and dot plot.

Yield curve inversion, Source: Tradingview

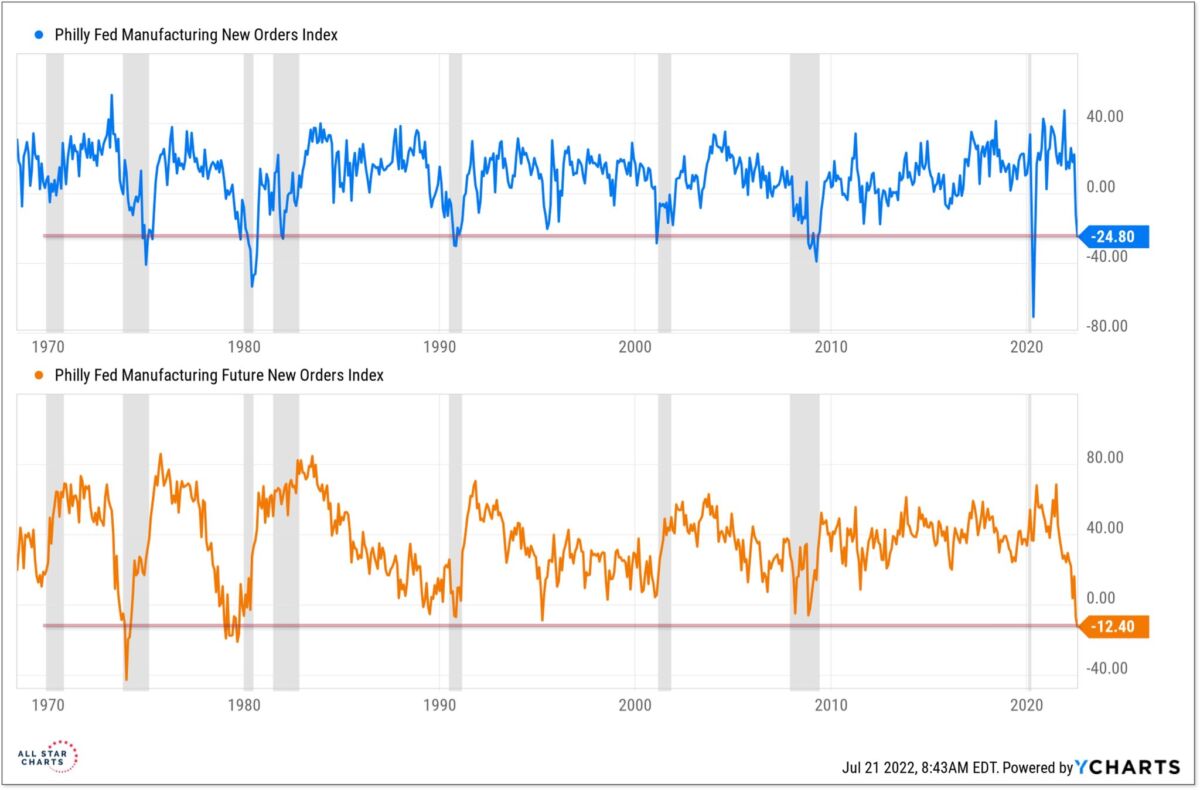

It also implies that the market is expecting a rate cut in the medium term. Now let’s look at recent news orders and future new orders indexes from the Philadelphia Fed in manufacturing. Both indicate recessionary levels and can be considered as leading indicators. The Fed will hike in this environment.

Philly fed manufacturing new and future new orders, Source: All starts charts via Ycharts

Inflation (CPI) vs. inflation expectations and the FOMC meeting

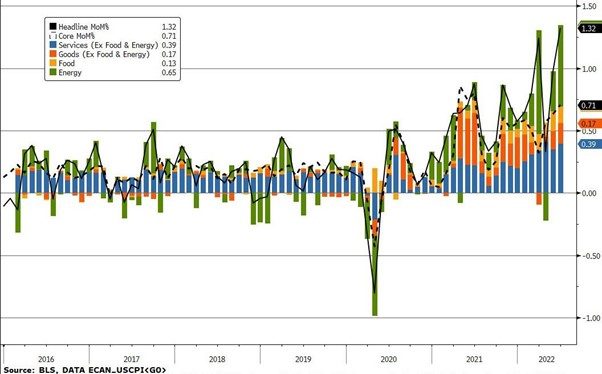

The real issue here is the inflation rate. However, the Fed wants to see a deceleration in the monthly inflation rate. It is not so easy and not so fast. Yes, the monthly, as well as YoY inflation rate, is rising, but the CPI is a very lagged indicator. For further inflation figures, it is much better to look at medium-term or short-term inflation expectations. The headline CPI MoM % inflation rate rose in June by 1.32%, while the core MoM % inflation rose by 0.71%. Both are very great prints but did not fully count the commodity drawdowns, mainly from the end of June.

Read also: Gazprom will shut down another turbine at Nord Stream 1

Headline and core inflation (MoM), Source: BLS via Zerohedge

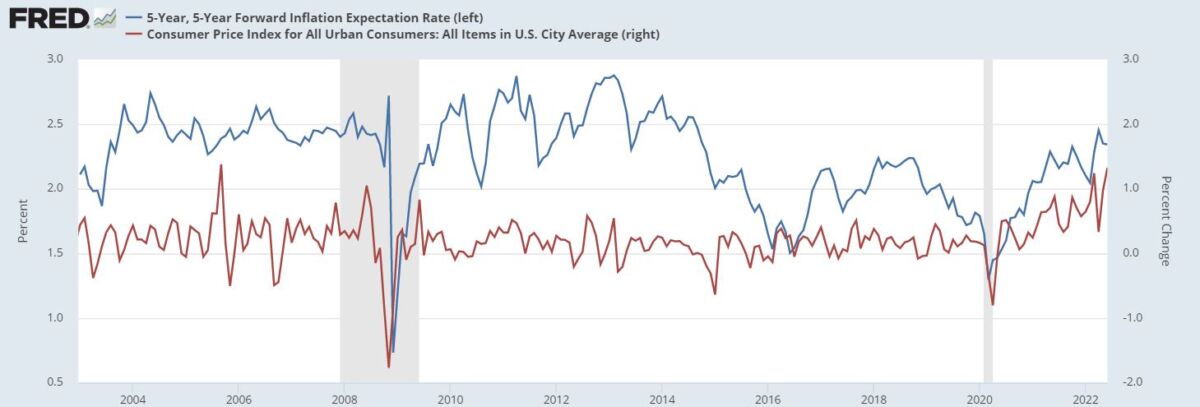

And in the next chart, we can see the relationship between 5y5y forward inflation expectations and the MoM % change in inflation rate. Forward inflation expectations are leading. However, here we can see how the CPI has lagged for many months as well as the job report. If the Fed acts on behalf of CPI prints, especially record prints, we can expect a policy blunder. Why? Because many leading indicators suggest an economic slowdown or recession and hiking more than currently market prices in is very dangerous. This week, the Fed will decide on further monetary policy moves. There are strong expectations for 75 bps or 100 bps hikes.

5y5y forward inflation expectatitons vs. CPI MoM % change, Source: FRED

But what the market currently prices in before the meeting? There is a relatively large chance of a 75 basis point rate hike and a smaller chance of the Fed delivering a 50 or 100 basis point hike. In our point of view, a 100bps is not out of the table, but it would be very aggressive, and we do not believe the Fed will react as aggressively to the upcoming economic slowdown/recession despite a strong labor market.

You may also like: Ryanair posts profit after 3 years

Trading idea

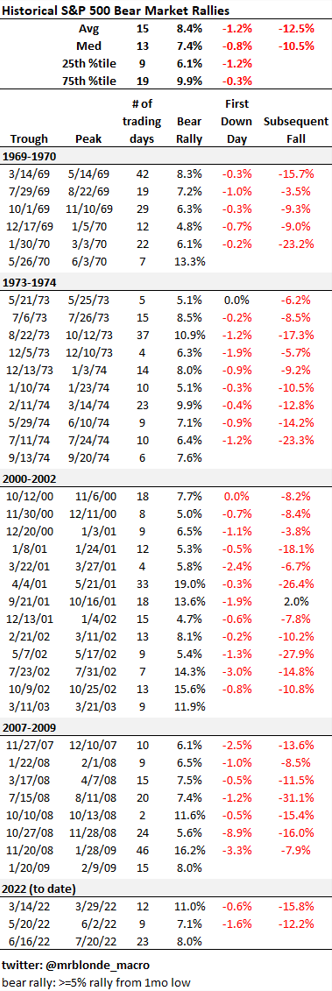

The best way to look at the market is to wait for FOMC results as well as Powell’s speech and watch out for his rhetoric. It will be crucial for the stock market as well as the bond market. However, there are plenty of signals suggesting an economic slowdown. The EPS should fall slightly, as indicated by the PMI, new orders, and other indexes. It is not a great time for the stock market right now. However, we can be wrong. We still assume that dovish rhetoric from the Fed can cause a bullish rally on stocks. However, as the cycle with EPS and revenue drop in guidances started, we are still neutral but slightly inclined to the opinion, we are in a bear market rally. The best way to fight this is not being long or maybe building only a really long-term position. However, the bonds with long-term maturities are much safer right now. We are still bullish on bonds with great maturities > 10 years and bearish on oil. We are watching the stock market closely, but we need to wait for some confirmation.

Historical S&P 500 bear market rallies, Source: @MrBlonde_macro

Comments

Post has no comment yet.