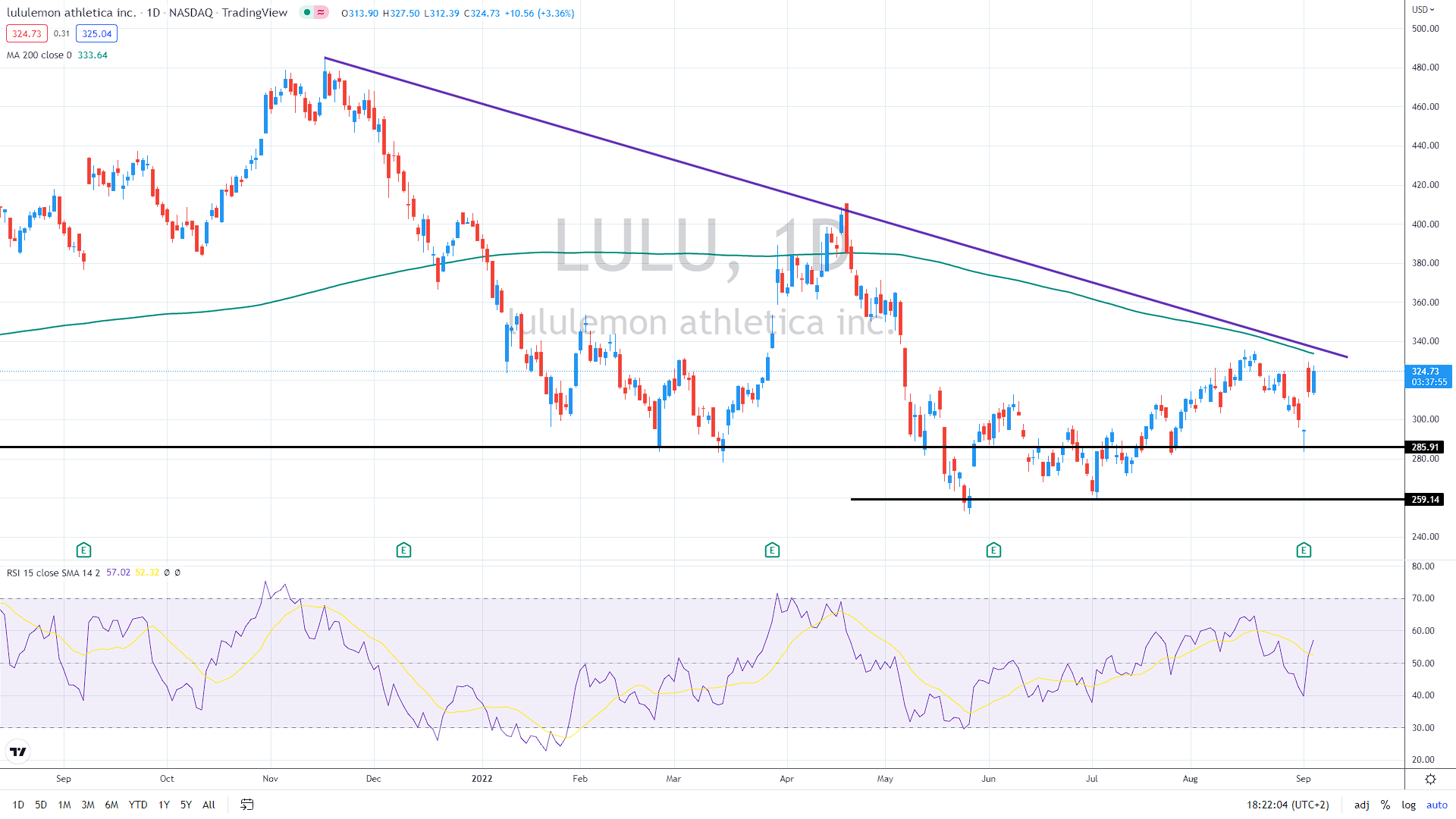

Lululemon Athletica remains one of the few fundamentally strong companies, delivering substantial growth over the previous quarters. Nevertheless, the stock remains below the bearish trendline, limiting its upside potential.

Solid earnings

On $1.87 billion in sales, Lululemon announced fiscal Q2 GAAP profits per share (EPS) of $2.26. The profits result exceeded expectations by 21%, or 39 cents. The revenue exceeded consensus by 5.6% and was above expectations by $100 million.

Related article: NVIDIA falls like a stone, and problems mount

The firm now has 600 locations globally after adding 21 net new stores during the quarter. Additionally, online sales increased 30% YoY and now make up roughly half of the overall income.

“Overall momentum in our international business remains strong, with revenue increasing 35% versus last year and 40% on a three-year CAGR basis,” said Lululemon CEO Calvin McDonald.

After a sluggish start to the year in China due to closures connected to COVID-19 and capacity issues, the country has recently experienced a recovery. The company’s revenue increased by over 30% from the previous year and by almost 70% on a three-year CAGR basis. In China, LULU is still in its early stages of development.

Inflation is not a problem for LULU

A fxstreet.com analysis showed that the firm’s operating margin of 21.5% was 30 basis points higher year over year, while Lululemon’s gross profit margin of 56.5% was 40 basis points higher than the estimate. Investors could see from these data indicators that Lululemon is not only addressing inflation head-on but also outperforming it, something that very few of its rival apparel companies have been able to do this year.

Same-store sales increased by 23% YoY, which may be related to decreased consumer concerns about inflation but also shows Lululemon’s power over customers.

The management improved the outlook for LULU shares by providing positive Q3 forecasts. A tight range of $1.78 billion to $1.805 billion was provided for the revenue forecast, while EPS between $1.90 and $1.95 was also higher than anticipated. This would result in revenue growth of 23% YoY and an EPS increase of 19% YoY.

You may also read: AUD/USD ignores another significant rate hike

Once the resistance level near 335 USD (the bearish trend line converged with the 200-day average) is broken to the upside, we might witness a massive rally toward 400 USD.

Alternatively, the failure to stay above 285 USD might cause another leg lower, targeting 260 USD.

LULU daily chart, Source: Author´s analysis, tradingview.com

Comments

Post has no comment yet.