A mortgage is a significant financial choice with long-term consequences. A mortgage is a loan that allows consumers to borrow money from a lender (usually a bank) to purchase a property. In exchange for the loan, the borrower agrees to pay interest and make monthly payments over a predetermined time, often 15 to 30 years. The property acts as collateral for the loan since the property secures the loan. If the borrower defaults on the loan, the lender has the right to confiscate the collateral.

When is the best time to take out a mortgage?

Many factors, including the financial status, credit score, interest rates, and the current real estate market, determine the optimal timing to obtain a mortgage. Before submitting a mortgage application, evaluating the financial condition and establishing whether the borrower can afford the monthly payments is crucial.

In addition to determining whether or not the person qualify for a mortgage, they need to check their credit score, also influences the interest rate they will pay. A higher credit score will result in a lower interest rate, resulting in lesser interest payments throughout the life of the loan.

Don’t miss: Credit Suisse ends up being bought by UBS for a bargain price

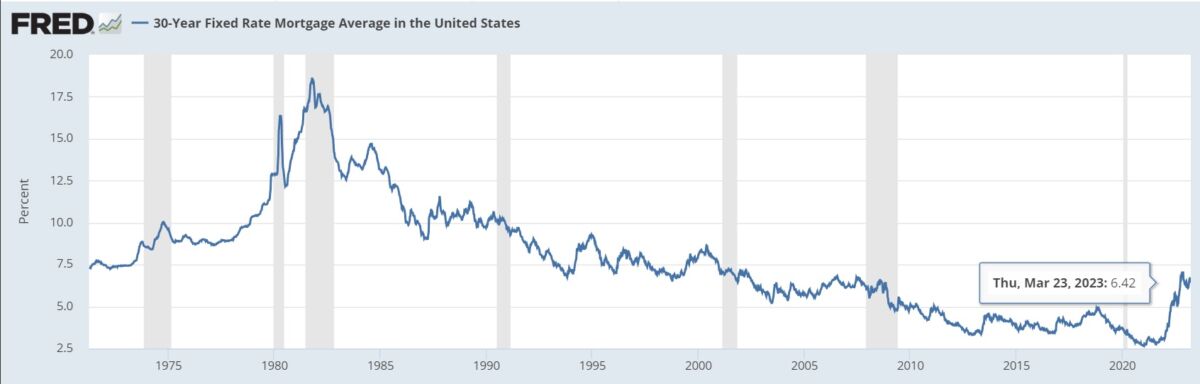

The interest rate is another crucial consideration when obtaining a mortgage. Many economic variables, such as inflation, the Federal Reserve’s monetary policy, and market circumstances, influence the fluctuation of interest rates. When interest rates are low, it may be advantageous to obtain a mortgage since the borrowers will pay less interest throughout the life of the loan. But, when interest rates are high, delaying taking out a mortgage and saving more money may be advisable.

30-year average mortgage rate chart, source: FRED

The present real estate market is another thing to consider. When the property market is thriving, it may be difficult to find cheap properties, and prices may be higher than typical. In contrast, housing prices may be lower during a recession or economic crisis, making it an ideal opportunity to acquire property.

What does it mean to take out a second mortgage?

A borrower who takes out a second mortgage obtains a second loan secured by the same property as the initial mortgage. In other words, it is a loan in which the borrower uses their residence as collateral to receive more cash.

The second mortgage is often taken out when the borrower needs additional funds for a considerable cost, such as home upgrades, education fees, or debt consolidation. This loan is in addition to the principal loan used to purchase the home, which is the first mortgage.

A second mortgage may be structured as a home equity loan or a home equity line of credit (HELOC). A home equity loan is a one-time, lump-sum payment repaid over a particular time, often between 10 and 30 years.

In contrast, a HELOC is a line of credit that permits the borrower to take funds as required, up to a pre-approved credit limit. Throughout the draw term, typically ten years, the borrower pays just interest on the amount borrowed and may repay and borrow again as required.

Another exciting topic: Stunning insights from Warren Buffett´s letter to investors in 2023

Note that taking out a second mortgage puts the borrower’s house in danger if they cannot make payments. If the borrower fails on the loan, the lender may foreclose and sell the property to recoup the unpaid amount. Therefore, before taking out a second mortgage, borrowers should carefully assess their financial status and capacity to repay the debt.

How to obtain a mortgage

Getting a mortgage is a significant financial decision, and the procedure might first appear daunting. However, with proper planning and preparation, it is possible to manage the process effectively.

Establishing a budget is the initial step in acquiring a mortgage. This entails analyzing income, spending, and debts to decide how much one may borrow. There are many online mortgage calculators to estimate potential monthly payments based on various interest rates and loan terms.

After establishing a budget, it is essential to verify the credit score. The credit score will significantly affect the mortgage’s interest rate and conditions. Therefore, when applying for a mortgage, one should take actions to enhance their credit score if it needs to be improved.

Next, compare banks to discover the best rates and conditions. One can compare rates from several lenders to determine what options are available. To apply for a mortgage, the borrower must supply information about the income, assets, and liabilities after identifying a lender. Before owning the new home, the borrower must sign the loan paperwork and pay any closing fees if they are accepted for a mortgage.

Comments

Post has no comment yet.