Overview

An extremely weak liquidity situation is a signal to investors that dilution is likely. The long-term trend of financial leverage continues to deteriorate, and banks may no longer finance such a corporation. COVID-19 hit the business model, while current macroeconomic conditions gave another hit, both with lowered consumer demand and worse conditions for debt refinancing.

Debt service consumes all EBITDA. If the company cannot start earning money soon, it will be forced to dilute its shares, which will significantly harm stockholders. The company is overvalued from both a historical standpoint and in comparison to its primary competitor.

Read also: Nasdaq tumbles after US jobs data, Gazprom halt

The business model will be hard to sustain. This is our conclusion after evaluating the financial perspective of RCL. We attempted to assess the financial health. However, COVID-19 had a devastating effect on the company. COVID-19 and all of the constraints that authorities imposed on cruisers were excruciating and ruined the entire business model. Expensive valuation criteria further reinforce the bearish thesis.

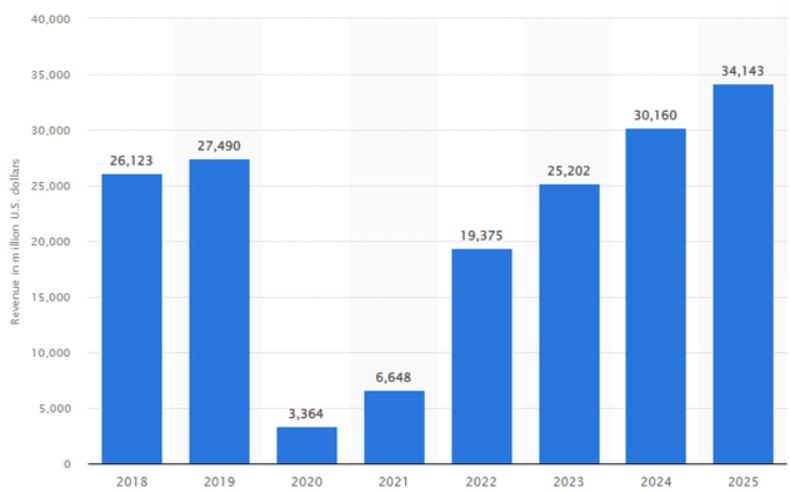

Revenue of the cruise industry worldwide from 2018 to 2025, Source: Statista

Only a small percentage of past cruise enthusiasts returned for this type of vacation (2020–2021). After the COVID-19 limits, many individuals altered their minds, and these customers are likely irrecoverable. According to the chart above, the sector’s revenue for the period 2020-2021 was terrible. However, projections for 2022 and 2023 are overly optimistic because the model doesn’t really account for global consumer destruction driven by high inflation and monetary tightening.

These companies in such industry took out so many loans on their balance sheets that their cash positions were mostly depleted and a significant number of them experienced dilution. The company’s liquidity and its ratios have never been worse, yet its leverage position is at its highest and most perilous level. In our view, the outcome will be either increased leverage or dilution, both of which are detrimental to shareholders. In addition, the current economic scenario is quite fragile.

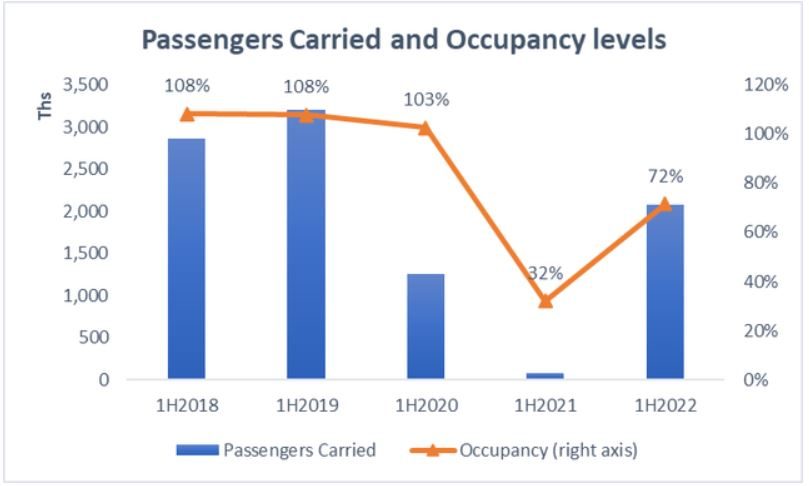

Additionally, “passengers carried” and “occupancy” levels confirm these facts. Both data indicate that we are at a three-year high, but we are still far from the 1H2019 levels. In prior years, occupancy rates exceeded 100 %, supporting the bullish business model hypothesis. Nonetheless, when COVID restrictions were implemented in 2020, passenger and occupancy numbers decreased drastically, and the company began to burn money.

You may be interested in: Russian foreign exchange reserves in Chinese yuan?

Nonetheless, even if the company reaches 80-90% occupancy, it would probably not be enough to fund basic operations, payments, and interest as it devours the remaining margins. If the company is unable to generate the same amount of EBITDA as in prior years, we believe that stock dilution will be imminent.

Carried passengers and Occupancy levels, Source: Investro analytics team via 10-K (RCL)

Liquidity focus

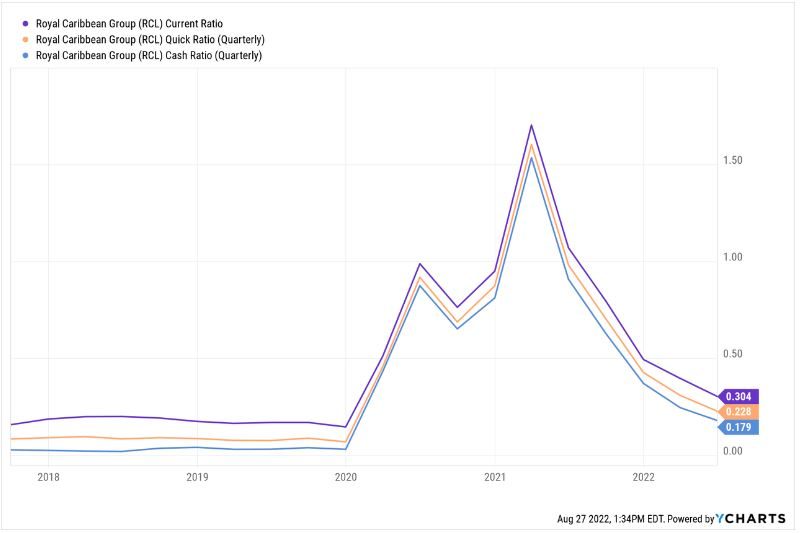

First and foremost, it is necessary to examine the present liquidity ratios of RCL. However, we are somewhat above the pre-COVID figures for all three ratios: current, quick, and cash ratio. It is deceptive. Even in 2019/2020, these ratios were extremely risky, and they do not fulfill the investable criteria since they pose a financial threat if the economy breaks down.

The company incurred much more debt due to COVID-19 (no revenues), with this severe blow increasing its liquidity ratios dramatically. We all believed it would be a temporary time span that cruises could easily endure. The liquidity flood in the markets was secured by the Fed and the government.

As the situation has not reached pre-COVID levels in terms of revenue and EBITDA, in our view, it is a foregone conclusion that the company will experience liquidity and solvency concerns, given that its liquidity ratios are only slightly above pre-COVID levels.

Before COVID, the situation was manageable due to sufficient income streams and EBITDA levels. However, due to the drastic shift in consumer behavior, the corporation cannot create new revenue streams or revitalize the old ones. In absolute terms, cash has significantly increased relative to prior years (primarily due to loans), but relative comparisons are the most objective and transparent (because debt significantly increased).

In the event of a lack of liquidity, shareholders are in a very precarious position because such ratios signal that management may be compelled to accept another portion of the loan, which is questionable owing to the company’s high leverage or more rational step-process through dilution.

RCL – liquidity ratios, Source: YCHARTS

Thoughts on stock dilution

RCL chart, source: finviz.com

Both directions are extremely risky for the corporation and its owners. We believe that the second option, stock dilution, will be extremely detrimental to shareholders because the value of their stock could decrease. However, it would be beneficial for the company’s financials and boost its likelihood of survival, but it would have a negative impact on price development.

At some point, though, the creditors may declare, “Enough is enough; we will no longer finance this.” The only way to finance the business model and its loans plus interest would be to issue notes or dilute equity.

Read more: G7 agrees to cap Russian oil prices

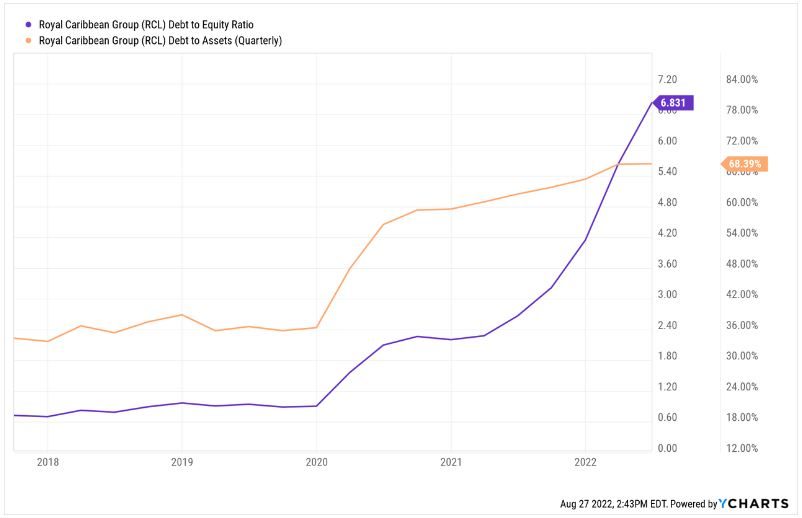

However, there is a significant distinction between loaded debt and leverage. If equivalent liquidity ratios existed in the pre-COVID period, the debt-to-equity ratio was between 0.70 and 0.90, and the debt-to-assets ratio was only between 35% and 40%. Currently, debt to equity is dangerously close to 6.8 and stands debt to assets at 68%. We are convinced that any bank funding will be extremely limited and dangerous for these institutions, as the company is now overleveraged and its debt is nearly entirely covered by its assets.

From this perspective, it is quite probable that the corporation will have to dilute its shares and issue further notes. Both approaches would be extremely risky for stockholders because there is no such thing as an abundance of free liquidity, as we observed in 2021 through periods of quantitative easing and fiscal stimulus. As a result of the Fed’s extreme hawkishness, the market is now confronted with a liquidity contraction. The stock price could be affected in a huge way by these necessary but difficult decisions made by management.

Debt to equity and debt to assets ratio, Source: YCHARTS

In the 2Q, there is more than 23 billion USD in debt, and debt maturing in 2022 and 2023 is a total amount of 7.32 billion USD. However, RCL agreed with Morgan Stanley about the partial refinancing of maturing debt:

“In June of 2023, approximately $3.2 billion of long- term debt will become due. Accordingly, in addition to our $3.3 billion liquidity as of June 30, 2022, in February 2022 we entered into certain agreements with Morgan Stanley & Co., LLC (“MS”) where MS agreed to provide backstop committed financing to refinance, repurchase and/or repay in whole or in part our existing and outstanding 10.875% Senior Secured Notes due 2023, 9.125% Senior Priority Guaranteed Notes due 2023 (the “Priority Guaranteed Notes”), and 4.25% Convertible Notes due 2023. Pursuant to the agreements, we may, at our sole option, issue and sell to MS five-year senior unsecured notes with gross proceeds of up to $3.15 billion at any time between April 1, 2023 and June 29, 2023, to refinance the aforementioned notes.”

According to 10-K:

As of June 30, 2022, we had liquidity of $3.3 billion, including $0.5 billion of undrawn revolving credit facility capacity, $2.1 billion in cash and cash equivalents, and a $0.7 billion commitment for a 364-day term loan facility available to draw on at any time prior to August 12, 2022.

EBITDA is insufficient

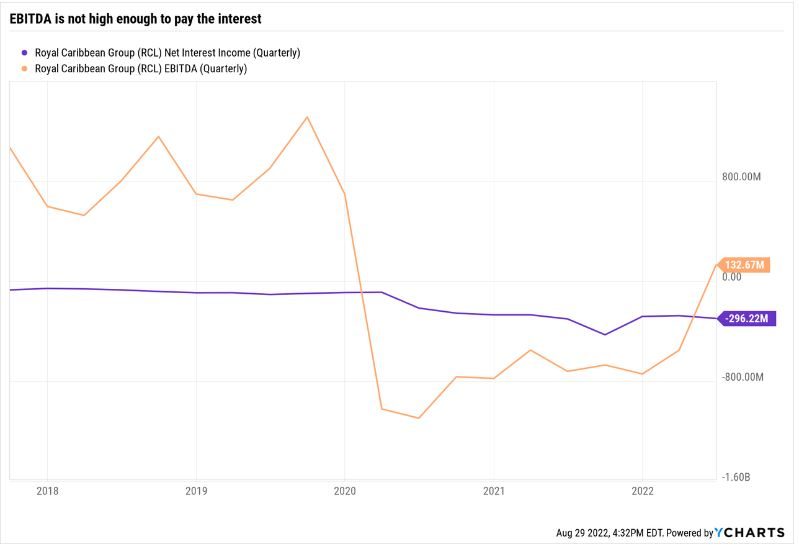

There are numerous financial concerns. The company has short-term liquidity, but it is in a very precarious position. In 2020, only interest payments were greater than EBITDA. Even if EBITDA reached a positive number (as the latest), it would not be sufficient to support basic operations. However, what about payments, debt maturity dates, and other cash outflow activities? If EBITDA does not return to pre-COVID levels quickly, which I do not believe will occur, the company could run out of cash, even using the “undrawn revolving credit facility.”

EBITDA is not high enough to cover interest payments, Source: YCHARTS

Under the current conditions and EBITDA figures, such a substantial portion of debt and interest is not manageable over the medium and long term in our opinion. It is notable in cash accounts as well. Consider the cash deceleration beginning in 2H2020.

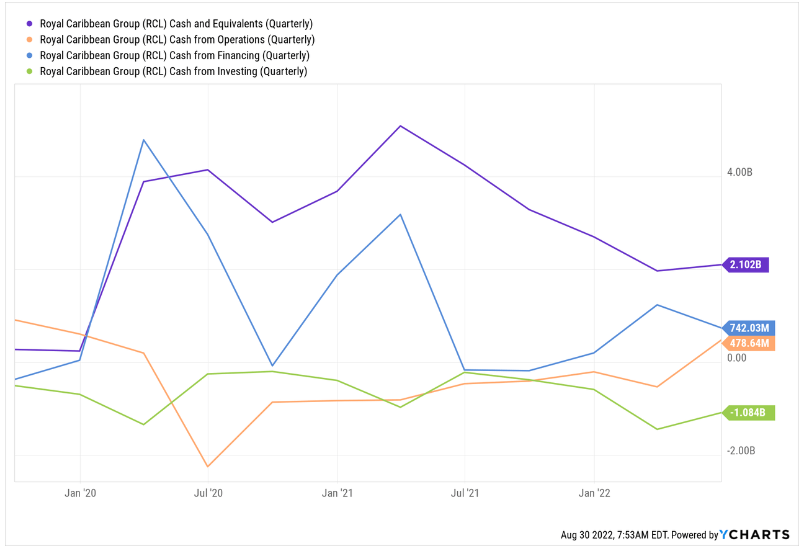

The subsequent chart illustrates that EBITDA generation has not been the key driver of cash growth. RCL is not generating reliable revenues for objective reasons, and CAPEX, basic operations, installations, and interest are financed by further loans, multiple credit arrangements, notes, and stock dilution. The Morgan Stanley arrangement now only covers the partial refinancing of maturing assets due in 2023. This firm relies on high CAPEX, which is difficult to reduce.

RCL – cash flow and cash balance (quarterly), Source: YCHARTS

Despite the inflow of cash from financing in the first quarter of 2022, cash and cash equivalents fell. The company must witness a large and rapid growth in cash flows from operations from the end of 4Q2022-1Q2023 under the baseline scenario to be successful. Otherwise, it can experience difficulties in surviving. This tendency will continue, in my opinion, because the global macroeconomic conditions are deteriorating and consumer spending is being severely impacted. The company is likely to survive, but its shares could be severely affected because it will have no other option for raising capital.

Valuation

There are numerous ways of evaluating that we may employ. Assessment based on stock price and tangible book value per share may provide the greatest fit under current market conditions. We would prefer the DCF technique of valuation, but the sector’s revenue growth is now unquantifiable. It could result in substantial deviation from the intrinsic value. The tangible book shows exactly how much the investor would have gotten back if the company had been shut down. It is the best choice in the current situation, given that the company has taken on so many loans on its balance sheet, and this valuation tool fits great to asset-heavy companies.

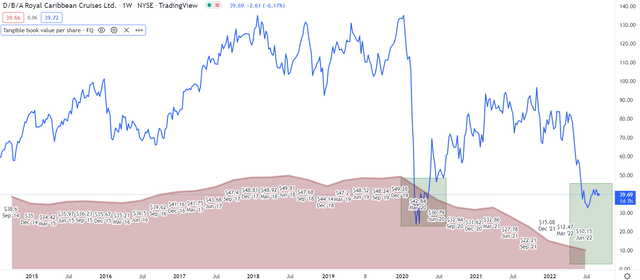

RCL, tangible book value, Source: Investro analytics team via Tradingview

At 10.15 USD, (RCL) tangible book value per share is at a multi-year low not seen since the 1990s. However, the price multiple declined marginally from 2020. It was an excellent idea to purchase shares of the company, because the stock was less expensive than its TB value.

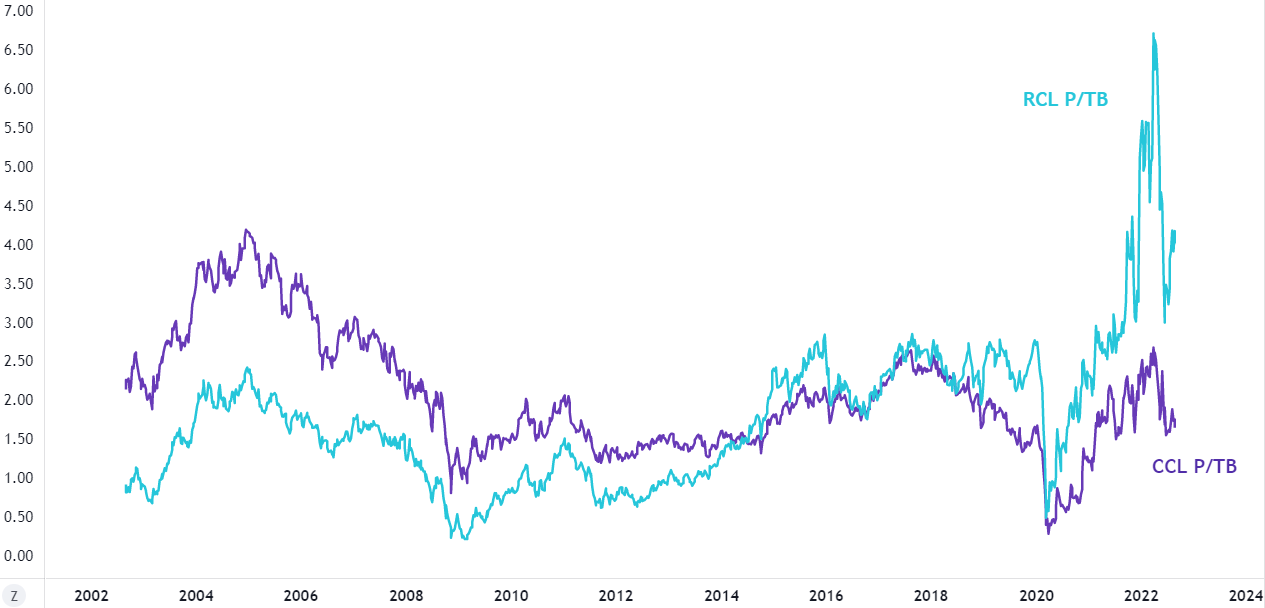

Since then, the value of TB has decreased dramatically as a result of the business model’s unsustainable use of leverage and the huge reduction of equity on the balance sheet. The current trading multiple hits an expensive 3.9, which is significantly above the historical average and median and below the stock’s all-time high from the preceding months. Comparatively, CCL as a comparable company in the industry appears significantly less expensive, as its multiple reaches only 1.6, which is below its long-term average and median. There are better-valued companies in this industry with lower debt levels.

Price to tangible book of RCL and CCL, Source: Investro analytics team via Tradingview

However, we often do not favor TB value as a criterion for valuation. We cannot use P/S, P/E, or DCF modeling to determine the intrinsic value or DCF value per share given the current circumstances, in which we do not have accurate and reliable forecasts of future revenues.

This time and under the current market conditions, we choose tangible book value as a wonderful instrument for determining the proper price at which to purchase its shares. From a historical standpoint, the firm could be added to the watchlist if its share price falls between $8 and $20, but its tangible book remains intact. However, as the company’s balance sheet is shaky, we have serious doubts that these conditions will be met.

Macroeconomic outlook

We will now outline a concise macroeconomic outlook. If you want more information, you may visit our weekly macro reports, in which we reveal the perspective on the monetary outlook and other macroeconomic relationships are presented in greater depth. Firstly, if loan interest is not hedged, rate increases will create substantial problems as debt service becomes more expensive. The company does not match several of the investment criteria. This is not due to weak revenue growth or limited cash flows, both of which could be temporary, but to a very unhealthy balance sheet.

Secondly, fuel prices are also extremely high, which contributes to the decrease in EBITDA margin. Once again, it is a pure loss if a corporation does not use the hedging strategy. The following factors are inflation and labor cost increases. The huge increase in inflation will result in increased employee demands.

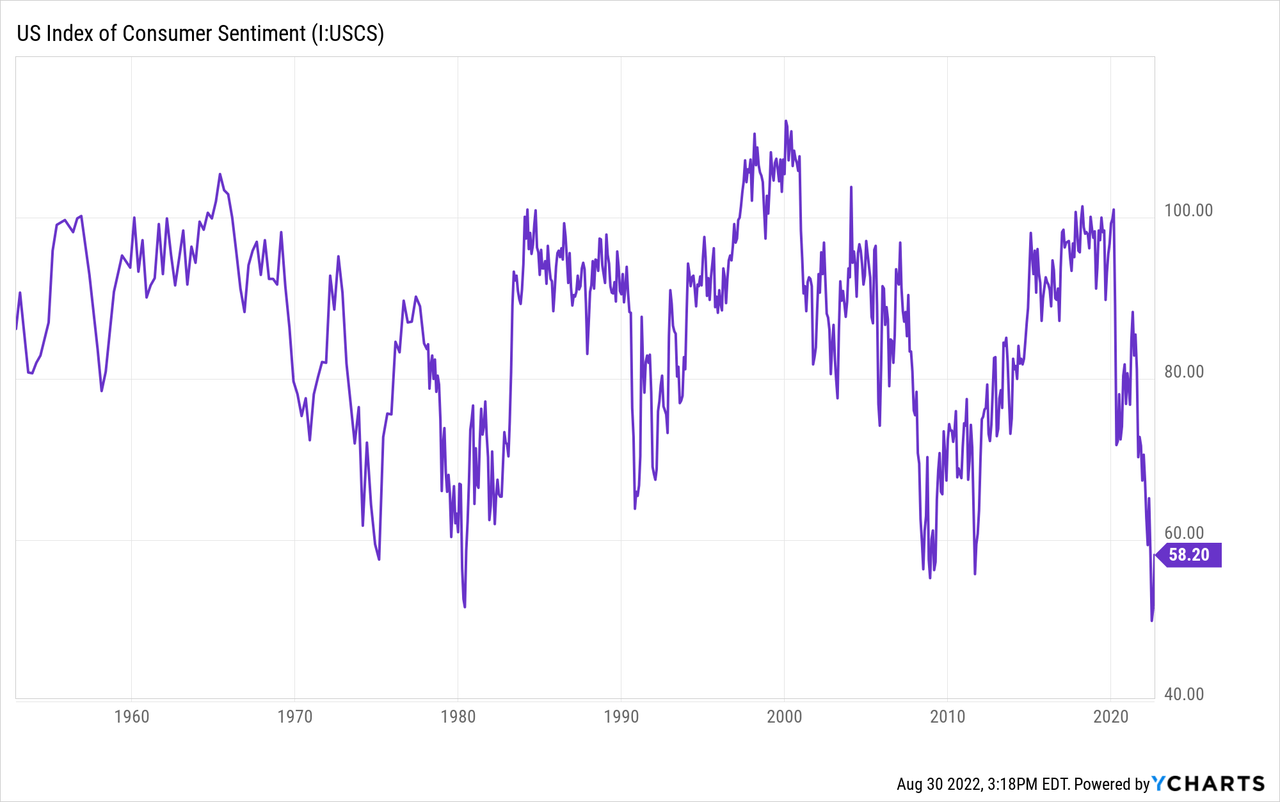

Consumer sentiment is also near a record low. Therefore, it is not an ideal time for recovery. Nonetheless, we may track the growth rate of bookings, but present macroeconomic conditions and poor consumer sentiment imply that strong results are unlikely. This is just a cyclical business where demand and mood play a big part.

US – consumer sentiment, Source: YCHARTS

Risks and Summary

We want to conclude first that we could be mistaken. We would be very astonished if people, vaccinated or unvaccinated, returned to cruises in a positive manner. It is possible that our EBITDA assumption is incorrect. Whether or not our thesis is correct, we are aware of one thing. RCL’s balance sheet is extremely weak and precarious. This analysis should give answers to the questions of whether the business model is sustainable, what the risks are, why the company’s shares are vulnerable and why the stock price is still overvalued.

In conclusion, we notice numerous red flags. However, the corporation or other cruise lines had comparable leverage at the time. Debt to equity and debt to asset ratios cannot be compared to now. Previously, despite poor liquidity, the company was able to manage problems with the external portion of its funding, and leverage was minimal. The current degree of financial leverage is extremely high and risky.

There is a limited opportunity for additional bank borrowing. The problems are also present in the financial market. As a result of a flood of money in 2020–2021, the company was able to issue notes with ease and obtain excellent financing. Now, as a result of the monetary tightening, liquidity is leaving the markets. RCL is in its most desperate situation ever.

We are not claiming that a business cannot survive. We just wanted to highlight that the company’s financial health is deteriorating and that, due to limited bank financing, it will be compelled to dilute its stock in order to raise funds for basic operations at a reasonable cost. Due to the lack of EBITDA creation and the need to maintain CAPEX, the business is quickly burning cash. In the preceding two years, only interest payments had exceeded EBITDA generation.

It changed in the most recent quarter, but it will not be sufficient for payments and other operations. The problem extends beyond disrupted company structures and revenue streams. The most significant concern is a very poor balance sheet, so a potential investor would need to be under constant pressure to determine whether or not the company can handle it.

However, due to the combination of nonreturnable customers and a deteriorating macroeconomic outlook, we do not expect the company will soon generate substantial revenue. In addition, refinancing conditions have deteriorated dramatically, and the company will no longer be able to refinance under acceptable terms, but only under essential terms, due to higher rates.

You may also like: Our latest weekly macro report and the outcome from Jackson Hole

Due to a shortage of funding, still dropping cash on cash accounts, and limited growth potential, there is a strong probability that the firm would dilute its shares in the medium term to address such a challenging scenario. Moreover, the stock is significantly overvalued from a historical point of view as well as to its main competitor. We believe that under current conditions, the investment climate is very unattractive. There are numerous superior investing alternatives available on the market.

Warning: The fully covered text is not investment or trading advice. It represents only the author’s point of view and thoughts, and we do not bear responsibility for your potential loss. The article serves only for analytical and marketing purposes.

Comments

Post has no comment yet.