Today we bring to you the most important summary from the FOMC Minutes released in the previous week. Minutes revealed some great insights from the June Federal Reserve FOMC statement:

Staff Economic Outlook:

“The projection for U.S. economic activity prepared by the staff for the June FOMC meeting implied a trajectory for real GDP that was lower than in the May projection. The staff continued to project that GDP growth would rebound in the second quarter and remain solid over the remainder of the year. However, monetary policy was assumed to be less accommodative than in the previous projection, and the recent and prospective tightening of financial conditions led the staff to reduce its GDP growth forecast for the second half of 2022 and for 2023. Labor market conditions also were expected to remain very tight, albeit somewhat less so than in the previous projection.“

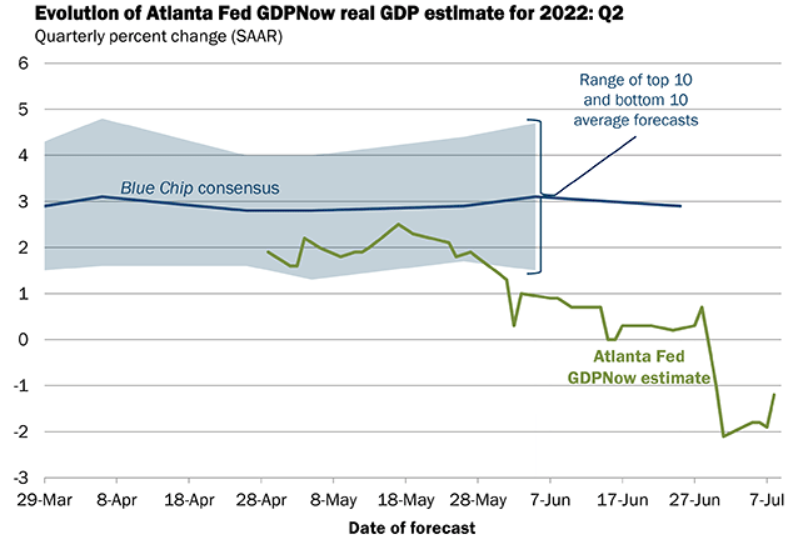

Our commentary: In our previous report, we confirmed that the new real GDP forecast for Q2 had been revised downward, pointing to the possibility of an economic slowdown. Additionally, this is indicated by weak consumer activity and other leading indicators (PMI). Although we talked about the labor figures in the latest macro report, it is still quite strong, which gives FOMC the room to feel more confident about delivering the additional rate hikes. Bear in mind, that Fed at FOMC Minutes with great certainty calculated with more optimistic figures (FOMC meeting at 14-15) as the most current leading indicators found the “turning-point” in late June and in July. On the other hand, the labor market remained strong, as we commented in our latest weekly macro report.

Source: Blue Chip Economic Indicators and Blue Chip Financial Forecasts, and Atlanta Fed

“The staff continued to judge that the risks to the baseline projection for real activity were skewed to the downside and that the risks to the inflation projection were skewed to the upside. The staff judged that the ongoing war in Ukraine remained a possible source of even greater upward pressure on energy and commodity prices, while the war and adverse developments associated with China’s zero-COVID policy were both perceived as increasing the risk that supply chain disruptions and production constraints would be further exacerbated in the United States and abroad.”

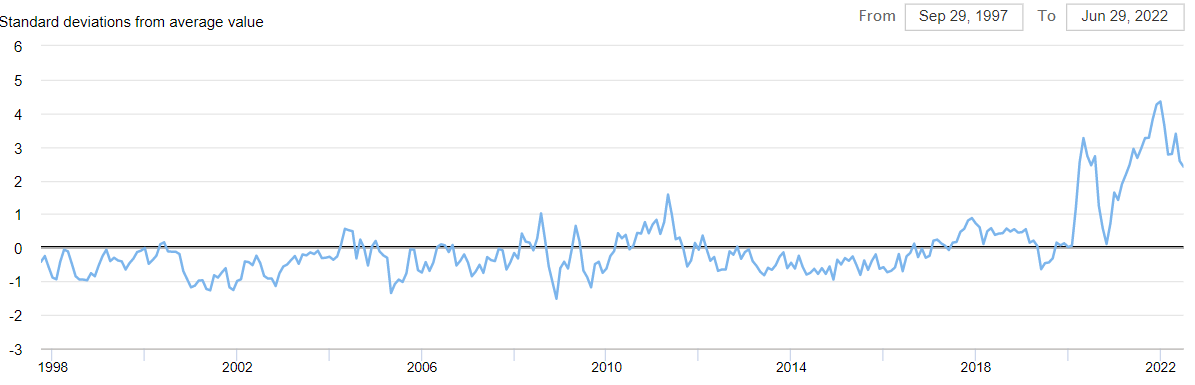

Our commentary: As a result of slower demand and concerns about a recession, commodity prices have continued in fall in recent weeks, reducing upside inflation risks. The price pressures on both food and industrial commodities have significantly decreased over the past few weeks and many of them are at pre-invasion levels. Only very slight decreases in Global Supply Chain Pressure Index means that supply chain bottlenecks might be less stressed, but still significantly deviated from the historical perspective. Lockdowns and China’s zero-COVID policy are also primarily behind us, which makes for another step toward easing of supply chain disruptions.

Read also: OECD plans biggest overhaul of cross-border tax rules

Global Supply Chain Pressure Index, Source: Bureau of Labor Statistics; Harper Petersen Holding GmbH; Baltic Exchange; IHS Markit; Institute for Supply Management; Haver Analytics; Refinitiv and other authors.

Participants’ Views on Current Conditions and the Economic Outlook

“With regard to the economic outlook, participants noted that recent indicators suggested that real GDP growth was expanding in the current quarter, with consumption spending remaining strong. Participants generally judged that growth in business fixed investment appeared to be slowing, and activity in the housing sector appeared to be softening, in part as a result of a sharp rise in mortgage rates. Correspondingly, participants indicated that they had revised down their projections of real GDP growth for this year, consistent with ongoing supply chain disruptions and tighter financial conditions. An easing of supply bottlenecks, a further rise in labor force participation, and the waning effects of pandemic-related fiscal policy support were cited as additional factors that could help reduce the supply– demand imbalances in the economy and therefore lower inflation over the next few years.”

“In their discussion of the household sector, participants indicated that consumption spending had remained robust, in part reflecting strong balance sheets in the household sector and a tight labor market. Participants generally expected higher mortgage interest rates to contribute to further declines in home sales, and a couple of participants noted that housing activity in their Districts had begun to slow noticeably. Against the backdrop of rising borrowing costs and higher gasoline and food prices, a couple of participants commented that consumer sentiment had dropped notably in June, according to the preliminary reading in the Michigan survey.”

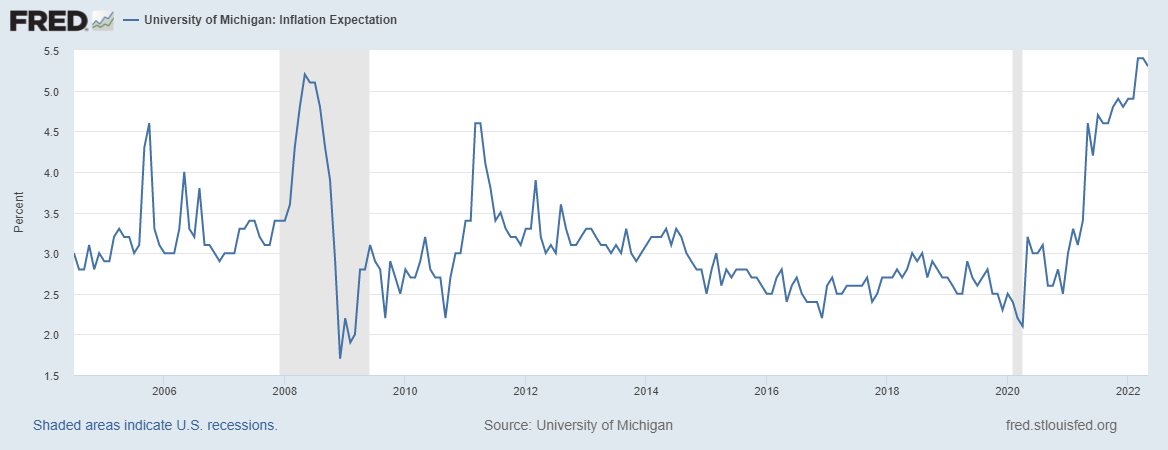

“Participants observed that some measures of inflation expectations had moved up recently, including the staff index of common inflation expectations and the expectations of inflation over the next 5 to 10 years provided in the Michigan survey.”

Our commentary: Financing conditions start to be very tight, mainly mortgage rates. Since consumer sentiment figures were worse than anticipated, consumer spending is currently suffering more. Although long-term inflation expectations for the next 5 to 10 years were lower than the preliminary results, which suggested a slight shift in participants’ sentiment, but inflation expectations are still significantly higher and elevated above the inflation target. University of Michigan results about 5-year inflation expectation ended 3.1% vs. 3.3% preliminary results for May.

UM: Inflation expectations, Source: FRED via University of Michigan

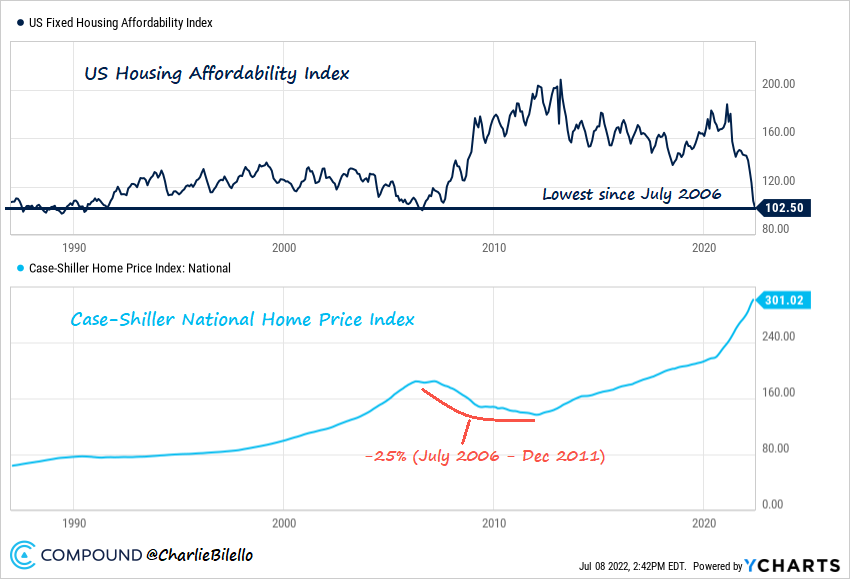

On the following chart from Charlie Bilello, we can see US Housing Affordability Index, which decreased to financial crisis lows in 2008-2009. After that home prices significantly decreased. We are at similar levels right now. It can lead to a further decline in home sales and maybe a stagnation or decrease in home prices as well.

You may like: Crypto news summary: Boris Johnson, Voyager and Celsius

“Most participants assessed that the risks to the outlook for economic growth were skewed to the downside. Downside risks included the possibility that a further tightening in financial conditions would have a larger negative effect on economic activity than anticipated. In particular, participants judged that an increase of 50 or 75 basis points would likely be appropriate at the next meeting.”

Our Commentary: We have discussed market pricing in detail in our latest macro report.

“Participants also judged that maintaining a strong labor market during the process of bringing inflation down to 2 percent would depend on many factors affecting demand and supply. Participants recognized that policy firming could slow the pace of economic growth for a time, but they saw the return of inflation to 2 percent as critical to achieving maximum employment on a sustained basis.”

Committee Policy Actions

“Members agreed that, in assessing the appropriate stance of monetary policy, they would continue to monitor the implications of incoming information for the economic outlook and that they would be prepared to adjust the stance of monetary policy as appropriate in the event that risks emerged that could impede the attainment of the Committee’s goals.”

Our Commentary: It is simple. Fed is aware of a further slowdown in economic growth but considers the return of inflation to 2 percent as a critical goal. In other words, only a weakening in the labor market or inflation slowdown can cause further ease of the aggressive tightening cycle. However, the inflation should slow down in 2-3 months, as many commodities achieve significant drawdowns. In the following months, probably we will face an inflation slowdown as a 5y5y forward inflation expectation decreased from June to 2.12. In summary, the Fed can not be as aggressive, because some inflation risks eased (will see after few months in CPI), and on the contrary, the downside risk of real economic activity increased.

5y5y forward inflation expectations, Source: macrotrends.net

Comments

Post has no comment yet.